The consumption of forest products continues to increase across the UNECE region, driven by the use of wood as a “greener choice” in building and energy use, and supported by favourable economic growth. However, trade restrictions are a growing challenge for the sector. These are the key findings of the UNECE/FAO Forest Products Annual Market Review 2016-2017, released today.

Wood products

The UNECE region – which is comprised of three subregions: Europe, the Commonwealth of Independent States and North America – recorded a continued increase in forest product consumption in 2016. This rise was led by sawnwood (+4.0), with the other two major primary product categories, panels, and pulp and paper also rising by 2.5% and 0.9% respectively.

For the first time in a decade, all three subregions showed growth in both production and consumption of sawn softwood. The improving economy, in particular related to construction and renovation, has played a strong role in this growth, but there is also increased momentum behind replacing carbon-intensive building materials with wood as a greener choice for building material, and using wood as a low-carbon source of energy.

Market trends

Market trendsMarket trends for 2017 point to continued growth across the region’s economies, particularly in Europe, where growth is accelerating. This is expected to boost the housing industry – a major driver of the use of forest products – where construction forecasts show increases for 2017 of 2-3%. Despite recent rises, construction remains 40-50% below pre-recession levels, which also highlights the scope for continued growth.

Trade developments

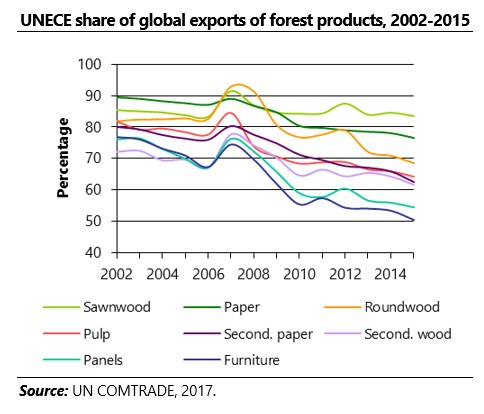

The UNECE region accounts for 60% of world trade in forest products although its share of export markets has been decreasing over the last decade. One of the major barriers to growth is the increasing level of restrictions on trade. As a recent example, a number of traditional log suppliers have imposed export restrictions designed to develop their domestic industry.

The most visible trade issue in the area of wood products is the US-Canada softwood lumber agreement, which expired in 2015 and is the object of intense negotiations. Currently the United States is planning to impose countervailing duties of 3-24%. One of the main elements of the allegations by the US Department of Commerce, and a basis for applied subsidy rates, is the issuance of log export restrictions on government-owned forestlands across Canada and, notably, on private lands in British Columbia (which is the leading sawn softwood-exporting province in Canada).

Wood products are subject to substantially more non-tariff measures than other manufactured products, which can have significant effects on their international trade. Examples include non-tariff measures intended to prevent insect infections, to assure the legal sourcing of timber, and to protect domestic producers. Such measures tend to increase costs for exporting countries in favour of domestic producers.

New products

New productsThere is an upswing in the use of cross-laminated timber, a relatively new product that has found expanded markets in wooden buildings, including large multi-story structures that had previously been dominated by concrete and steel construction materials. European production is around 680,000 m3 and is expected to rise to 1.2 million by 2020. The building industry is increasingly favouring the use of wood in construction, as can be seen in recent high-rise developments, such as an 18-storey wooden hybrid building at the University of British Columbia in Vancouver which was built four months faster than similar non-wooden buildings, reducing construction time by almost 20%. The potential market in the United States alone is seen as between 2 and 6 million m3.

Wood pellet consumption in the region is also at a record high of 25 million tonnes, up 4% over 2015 and more than 50% over 2012. In Europe, the increase was 6.6% for 2016. This densified energy product is a major factor in retaining wood’s status as the leading source of renewable energy in the region.

Certification

The two major certification schemes – the Forest Stewardship Council (FSC) and the Programme for the Endorsement of Forest Certification (PEFC) – reported a combined global total of 497 million hectares of certified forest in May 2017, representing a year-on-year increase of 35 million hectares (7.5%). However, nearly 69 million hectares are now certified under more than one scheme – a decline of 3 million hectares of certified forest area from the previous reporting period (which can largely be explained by overlapping certification of forestlands from both FSC and PEFC).

Trade flow tables showing international trade in wood products are available at: www.unece.org/DAM/timber/statsdata/trade-flow-fpamr2017.pdf

Florian Steierer

[email protected]

+41 22 917-1409

UNECE/FAO Forestry and Timber Section Forests, Land and Housing Division UNECE